Understanding Self-Funded Insurance Plans vs. MERP Products: Key Differences and Considerations

Table of Contents

Health insurance costs have been rising for years, and experts predict the trend will only continue. Many businesses are turning to other health insurance benefits, like self-funded health insurance plans and medical expense reimbursement plans (MERP)), to lower their spending.

Self-funded and MERP products are both employer-sponsored health plans under Section 105 of the Internal Revenue Code (IRC). Organizations can use them to reimburse employees for tax-free medical and health insurance expenses, and they are often more cost-effective than traditional insurance plans.

Explore the differences between self-insured plans and MERP products in this guide. You'll also learn how they compare to traditional, fully insured plans.

What Is Self-Funded Insurance?

Employers can offer self-funded or self-insured medical reimbursement plans instead of fully insured group health plans. With a self-funded plan, the employer runs their own health plan and covers healthcare claim costs for its employees as they occur. Some employers hire a third-party administrator (TPA) to help manage claims, payments, and compliance, but the employer remains in control.

By taking over employee health insurance, businesses assume the full financial risk of employee healthcare benefits. They're responsible for paying out eligible employee claims, which vary annually. If claims are lower than the assigned budget, the employer saves money.

However, high claims can strain cash flow and cause losses. To reduce this risk, employers can take out stop-loss insurance to receive protection for claims that exceed a specified amount.

Self-Funded vs. Fully Insured Plans

How do self-funded insurance plans differ from fully insured plans? A fully insured health plan — also called a group health plan — is a traditional form of insurance that businesses offer eligible employees. The employer usually splits a fixed premium with the employee and pays it to a group health insurance provider. The insurer then covers employee healthcare expense claims, but the employees may have to pay deductibles, coinsurance, and copayments.

Fully insured plans differ from self-funded plans in the following ways:

- Risk exposure: Fully insured group health insurance offers much lower risk, as the insurer is responsible for paying out employee claims. When employers choose self-funded insurance, they assume all risk and pay for employee health claims when they occur.

- Cost: The cost of fully insured health plans is predictable, thanks to fixed premiums. Self-funded insurance costs vary depending on the number of employee claims. Employers can potentially save costs with self-funded plans if employees make fewer claims.

- Complexity: Employers appreciate fully insured plans because the insurer handles all the administrative tasks, such as processing claims and making payments. Employers that choose self-funded insurance must manage these tasks themselves or pay a TPA to help them.

- Customization: Group health insurance providers usually offer structured insurance plans employers can choose from, and there's little room for customization. Employers have much more freedom to customize a self-insured plan to meet employer and employee needs.

- Tax savings: With fully insured plans, employers can deduct the premiums they pay for employees as a business expense, reducing their taxable income. Businesses with self-insured plans can deduct their employee healthcare claims and administrative costs as business expenses, too. Self-insured plans are also exempt from state health insurance premium taxes, which can save employers money.

What Is a Medical Expense Reimbursement Plan?

Through a MERP, employers reimburse employees for certain out-of-pocket healthcare expenses. These include deductibles, copayments, coinsurance, and qualified medical expenses. Most employers pair a MERP with a high-deductible health plan with lower premiums but higher out-of-pocket costs.

Employees can use their MERP allowance to pay for anything their insurance doesn't cover. Employers can offer stand-alone MERP products so employees can also use their MERP allowance to pay for individual health insurance premiums. The employer typically sets a reimbursement allowance for each employee to use for eligible expenses yearly.

Usually, the employee must pay for the healthcare costs themselves and then submit a claim to their employer. Another option is to give employees a MERP debit card to pay with their allowance directly.

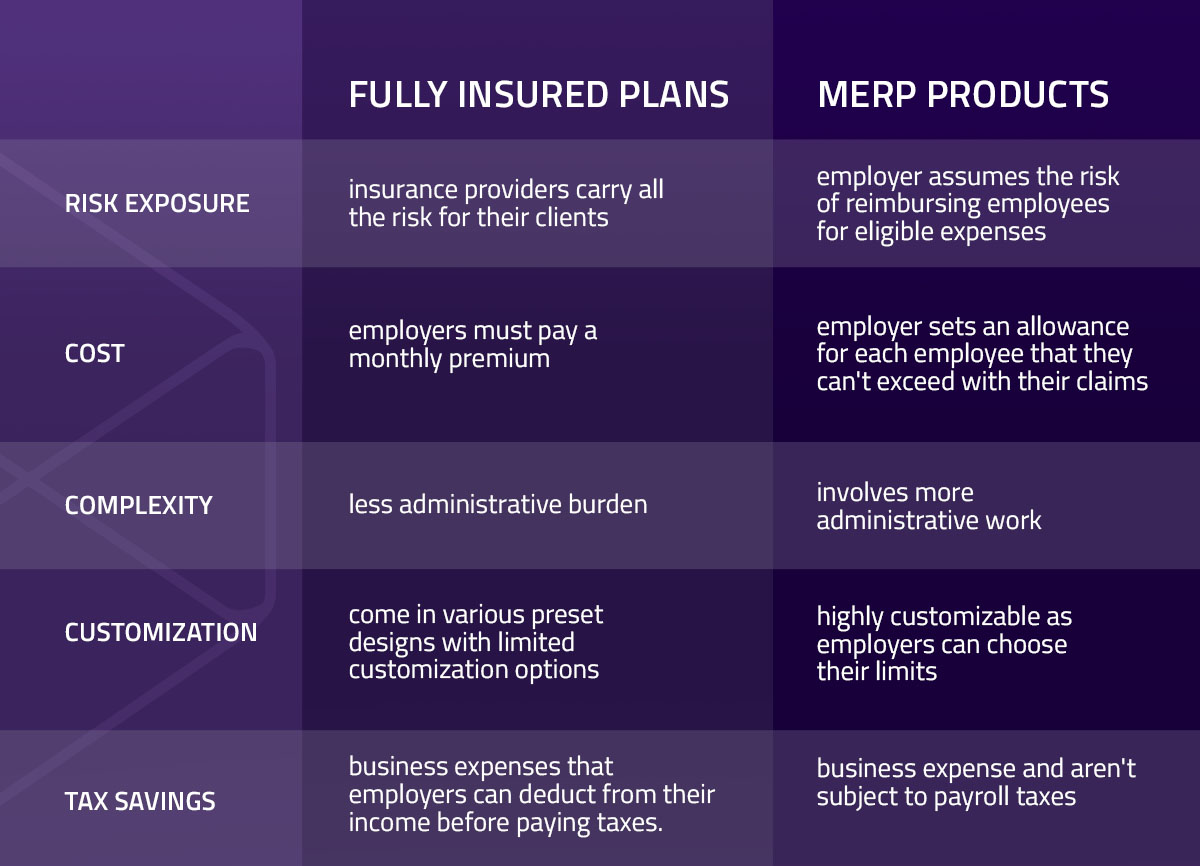

MERP Products vs. Fully Insured Plans

While self-funded insurance plans are similar in structure to fully insured plans, MERP products differ. A MERP is an employer-funded companion product to complete insurance, covering things the insurance plan doesn't. Fully insured plans require monthly premium payments and provide coverage for employees' medical expenses.

Other ways MERP products differ from fully insured plans include:

- Risk exposure: Insurance providers that offer fully insured plans carry all the risk for their clients, making them less risky for the employer. With a MERP product, the employer assumes the risk of reimbursing employees for eligible expenses. However, the risk is relatively limited as employers can set a threshold for reimbursement payments.

- Cost: Employers must pay a monthly premium to insurance providers to maintain fully insured plans, which makes the costs more predictable. MERP products are also predictable because the employer sets an allowance for each employee that they can't exceed with their claims. They can save money if employees don't use their full allowance.

- Complexity: Fully insured plans have less administrative burden because the insurance carrier does everything. A MERP product involves more administrative work than fully insured plans but less than self-insured plans. Employers can hire a TPA to handle MERP-related tasks.

- Customization: Fully insured plans come in various preset designs with limited customization options. MERP products are highly customizable as employers can choose their limits, which expenses they allow, and how to offer them.

- Tax savings: Fully insured plan costs are considered business expenses employers can deduct from their income before paying taxes. MERP reimbursements are also a business expense and aren't subject to payroll taxes, helping employers lower their payroll tax spend.

Comparing Self-Funded Insurance Plans and MERP Products

Self-funded and MERP products are Section 105 plans, but they work slightly differently. Consider the following when choosing between the two:

1. Structure

Self-funded insurance plans provide comprehensive health insurance to employees. Like a traditional insurer, the employer funds the plan and pays for claims directly. Employees will have a similar experience with a self-funded plan as with a group health plan. For example, they may still need to pay a premium to their employer and other out-of-pocket costs like copayments.

A MERP product supplements existing health coverage rather than replaces it. Employers contribute to the MERP to create a fund that reimburses employees for expenses their insurance doesn't cover. Employees must first pay for the expense and then claim from the MERP fund.

2. Risk Exposure

Self-funded plans require the employer to assume all risk for employee insurance claims. Some claims can be incredibly high, such as when an employee needs a serious medical procedure. Without stop-loss insurance, the risk may be too much for some businesses.

Offering a MERP is much less risky because the employer sets a specific allowance for each employee. Employees can claim for health insurance costs until they reach their maximum allowance. The MERP also only allows specific healthcare-related expenses that the employee's insurance doesn't cover, and the employer can choose which expenses to reimburse.

3. Cost

Self-funded insurance plans and MERP products are typically more affordable than traditional insurance as they don't require paying a premium to a third-party insurer. However, their cost to the employer varies. Self-funded plans are a little less predictable because claim amounts vary. They also cover a wide range of healthcare expenses and have demanding administrative requirements, which can raise costs.

A MERP often costs less than a self-funded plan because it's meant to work as an add-on. The employer can choose a lower-cost, high-deductible insurance plan and set a specific budget for the MERP allowance. The employer can better predict health benefit costs by paying a lower, fixed premium and having set MERP costs.

4. Customization

A self-funded plan offers a lot of flexibility and customization options for employers. They can design an insurance plan that fits their exact employee needs and budget and can make adjustments as needed. For example, employers can decide on what services to cover, the benefit levels for each one, and the amounts for out-of-pocket costs.

MERP products are also customizable. Employers can choose which expenses they reimburse and how much allowance to give employees. They can even choose to reimburse employees for expenses that traditional insurance doesn't cover, like over-the-counter medication, acupuncture, gym memberships, and vision exams. Employers can also decide how to offer MERP products, whether with a group insurance plan or on their own.

5. Complexity

Another way self-funded plans differ from MERP products is their administrative complexity. Self-funded plans carry high administrative burdens because the business must do everything an insurance provider would. They need an experienced team to complete these tasks while remaining compliant with health insurance regulations. Hiring a team or outsourcing administration can be complicated and costly.

MERP products are less complex because they only reimburse employees for specific expenses. Employers only have to worry about processing a smaller amount of claims and paying them out, usually by adding the funds to the employee's paycheck. They can also outsource this work to a TPA, reducing the administrative burden.

5. Regulations

Businesses that offer self-funded insurance must comply with more comprehensive insurance-related regulations, including:

- The Affordable Care Act (ACA)

- The Health Insurance Portability and Accountability Act (HIPAA)

- The Employee Retirement Income Security Act (ERISA)

- The Consolidated Omnibus Budget Reconciliation Act (COBRA)

- The Mental Health Parity and Addiction Equity Act (MHPAEA)

- IRC Section 105

MERP products may also have to comply with these regulations but often have less complex requirements. Complying with the IRC Section 105 rules is especially important for businesses to keep enjoying the tax advantages of MERP products and self-funded plans. For example, businesses must conduct nondiscrimination testing to ensure the plan doesn't favor highly compensated employees.

6. Suitability

Large businesses often find it easier to use self-funded insurance plans because they have a more stable cash flow and can handle the associated risk. They're also more likely to have sufficient administrative staff to handle the plan, compliance, and claims tasks involved. Smaller businesses may not have the financial resources to offer self-insured plans.

MERP products are more accessible to businesses of all sizes, even new businesses. In fact, small startups can use a MERP to help them provide more comprehensive health benefits to employees at a lower cost. Larger businesses can also use MERP products to save money without reducing employee health benefits.

7. Employee Benefits

Businesses offering self-funded insurance plans or MERP products offer employees various benefits. When an employer elects to self-fund employee health insurance, employees may receive more personalized coverage than traditional insurance. They may also have access to wellness benefits and preventive care that insurance doesn't usually cover.

MERP products have the potential to significantly reduce employee medical costs. While insurance covers many things, employees still have to pay for some expenses and out-of-pocket costs like deductibles. A MERP covers many of these extra costs, helping employees afford healthcare and relieving financial stress. If their employer allows it, employees can contribute to a MERP with pre-tax dollars deducted from their wages, saving them more for their medical expenses.

Reduce Employee Health Benefits Costs with The Difference Card

At The Difference Card, we know how expensive employee health benefits can be. We also understand how essential health benefits are for attracting and retaining top talent, and that's why we're dedicated to helping employers save money on health insurance.

We help businesses establish and implement unique MERP solutions to reduce costs without reducing their benefits package. On average, we reduce employer health insurance spending by 18%. We also take on the administrative responsibilities of MERP products and can set your employees up with a Difference Card Mastercard they can swipe to pay for some expenses directly.

As an insurance broker, you'll also benefit from offering The Difference Card solutions to clients. Our innovative solutions can help you stand out in a competitive market and reduce costs for your clients, helping you grow your business. In 2024, our partner agencies achieved over $8.4 million in new revenue.

Request a proposal from The Difference Card today!