Cost Saving Strategies for Brokers

Table of Contents

- 1. Prioritize Client Education and Communication

- 2. Implement Healthcare Benefit Optimization

- 3. Explore Low-Cost Group Health Insurance Plans

- 4. Offer Voluntary Benefits

- 5. Leverage Flexible Benefits

- 6. Combine Solutions for Maximal Value

- Partner With The Difference Card to Create Unbeatable Healthcare Deals

As an insurance producer, your pitch is most persuasive to prospects when you show them you can put together the benefits they need for their employees at the best price. Along with your expertise in finding solutions that align with their priorities, your ability to get your clients the best deals is core to your value proposition. As the cost of medical benefits rises 8-9% each year, the impact of cost-saving strategies will continue to increase.

The more you know about cost-saving strategies and the more established your track record of delivering on promised savings, the more you'll stand out from competing producers. Below are six cost-saving strategies to maximize the value your clients get from their healthcare spending.

1. Prioritize Client Education and Communication

Before diving into specific strategies you can bring into your offering to save your clients money, it helps to understand their expectations. Here are five tips to guide your communication with clients to boost their satisfaction with your solutions:

- Establish their budget: Ask your clients about their annual employee healthcare budget. Use their budget to inform which solutions to offer them for the most value. If they have yet to establish a specific budget or their numbers are unrealistic, this is an opportunity for your expertise to be a resource to them. Help them understand how much similar businesses typically spend and what benefits they can expect at different levels of investment.

- Discuss their priorities: Explore the healthcare benefits your clients would like to offer — they may need your advice in this area. Help them understand the extent of coverage they should offer to comply with regulations, attract and retain talent and enhance employee engagement. Explore any distinctive medical needs related to their industry's working conditions. Understanding their priorities and budgets will help you guide them and set realistic expectations.

- Support employee education: Your clients will get the best results from their coverage solutions when their employees know what they're signing up for. Position yourself as a helpful, expert partner in educating their employees about the company's healthcare solutions. Healthcare education can include helping employees to make decisions that lower costs for them and their employers.

- Share resources: Give your clients and their employees access to helpful resources like registration walk-throughs, quick-read info sheets and informative live webinars to reinforce their understanding of the solutions.

- Stay in touch: Regularly check in to ask how satisfied they are with their employee healthcare plan. Keep your finger on the pulse of any shifts in their priorities as budgets, regulations and industry landscapes evolve. Being available for constant support incentivizes your clients to continue working with you year after year.

Ongoing communication can help you foster long-term relationships with employers and anticipate their changing needs to boost satisfaction and mutual success.

2. Implement Healthcare Benefit Optimization

Healthcare benefit optimization is a data-driven approach to improve the value you can offer your clients. Through benefit optimization, you can save your client from overspending to solve problems their employees don't have. You can also help them identify gaps their healthcare solution should fill to attract, protect and retain employees.

Consider exploring software to gather and analyze data efficiently so it can inform your recommendations. Depending on the client, healthcare benefit optimization may involve:

- Identifying coverage overlaps where clients are spending twice for the same benefit.

- Finding gaps where employees lack coverage for eventualities that your client wants to address.

- Recognizing which benefits employees currently have access to but don't use.

- Ranking which categories of healthcare expenses employees incur most often.

- Tracking how benefits impact employee retention and engagement.

- Keeping up with regulatory requirements affecting your client's choice of healthcare solutions.

- Exploring the benefits competitors offer and opportunities for your client to compete for talent.

- Educating employees about health, wellness and how to use their benefits responsibly.

- Surveying what benefits employees want from their employer's healthcare solution.

- Comparing solutions to find the most affordable way for your client to offer optimized benefits.

3. Explore Low-Cost Group Health Insurance Plans

The go-to cost-saving solution for many producers is to help clients enroll in low-cost group health insurance plans. While carriers will offer companies lower premiums on all these plans, some plans are more affordable for employers than others.

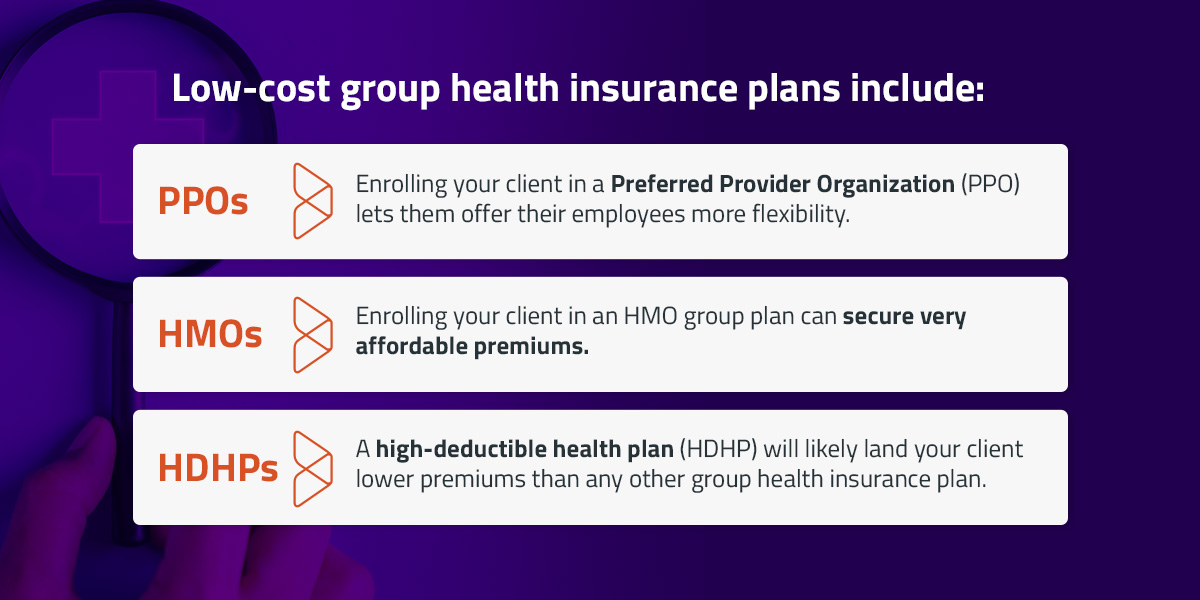

Low-cost group health insurance plans include:

- PPOs: Enrolling your client in a Preferred Provider Organization (PPO) lets them offer their employees more flexibility than some alternative group plans, like Health Maintenance Organizations (HMOs). Employees will enjoy the freedom to visit their preferred doctors and hospitals. On the other hand, PPOs will cost your clients more money and may not save their employees as much as some alternatives can.

- HMOs: Enrolling your client in an HMO group plan can secure very affordable premiums. At the same time, employees may feel limited by the network of covered providers.

- HDHPs: A high-deductible health plan (HDHP) will likely land your client lower premiums than any other group health insurance plan. These plans should be part of every producer's cost-saving toolkit. The trade-off is that employees will be responsible for higher deductibles and co-payments when they do need to claim. There are solutions to offset this cost for employees so that everyone wins. Keep reading for more on that.

Educate employers on these options and help them determine if PPOs, HMOs or HDHPs are appropriate for their workers' specific healthcare wants, needs and demands.

4. Offer Voluntary Benefits

Help your client implement customizable coverage solutions. You can support them by offering voluntary healthcare benefits on top of their core plan.

Popular voluntary benefits include:

- Vision

- Dental

- Life insurance

- Hospital indemnity

- Disability coverage

Many employees will appreciate optional access to these benefits, but your client can save money by excluding them from the default healthcare plan. Voluntary benefits can be entirely at the employees' expense, or your client could choose to contribute. Either way, they are an effective cost-saving solution that enhances employee satisfaction with various options.

5. Leverage Flexible Benefits

Your clients want to cover employees in impactful ways while saving costs. Their employees value having choices regarding their healthcare benefits.

Flexible benefits, including Health Savings Accounts (HSAs), Flexible Spending Accounts (FSAs) and Medical Expense Reimbursement Plans (MERPs), can serve both employer and employee priorities. These benefits efficiently maximize cost savings and employees' freedom of choice when working separately or with a low-cost group health insurance plan.

Health Savings Accounts

Health Savings Accounts are a great flexible healthcare benefit option that works together with an HDHP. Employees can use this account to contribute, grow and draw money for qualified medical expenses, all tax-free. Your client can contribute to this account as a tax-deductible business expense to offset their employees' deductible and co-payment costs when claiming from their HDHP.

Combining HSAs with HDHPs creates a win-win situation where employers keep their premiums low while supporting their employees' health, engagement and savings. Compared to FSAs, HSAs benefit employees by allowing funds to roll over and build up over their lifetime.

Healthcare Flexible Spending Accounts

FSAs are one of the most versatile ways for employees and employers to make tax-free contributions to cover employees' medical expenses. Unlike HSAs, which must be combined with HDHPs, FSAs can be used alone or with a range of other healthcare plans.

If your client is a large employer and wants to provide FSAs for employees, help them identify the right solutions to ensure they comply with the Affordable Care Act (ACA) minimal essential coverage requirements. Check if the FSA provider allows funds to roll over under any conditions, and communicate these to your client.

Employers and employees should understand that FSAs usually operate according to the “use it or lose it” principle, meaning funds do not build up year after year. With that in mind, FSAs are still a great way for employers and employees to save money while providing flexible coverage to offset medical expenses.

Medical Expense Reimbursement Plans

Medical Expense Reimbursement Plans may be the least well-known of the flexible healthcare benefit solutions in this article. But they are one of your best tools for saving your clients money while helping them contribute to the medical needs that matter to their employees.

A MERP allows your client to set the exact dollar amount they will reimburse an employee for annual medical expenses. They can either set a total limit and let employees prioritize their own spending on qualifying medical expenses, or they can stipulate different amounts for categories, such as:

- Emergency care

- Doctor appointments

- Prescriptions

- Over-the-counter medications

- Mental health care

- Vision care

- Dental care

- Menstrual care

- Ambulance transportation

- Co-pays

From there, employees can choose the healthcare services as needed. Your client will reimburse employees within their set allowance limits to cover eligible expenses. Partnering with the right MERP administrator can streamline approval and reimbursement for your client. This can involve implementing a MERP debit card pre-loaded with funds for eligible expenses. Any unspent funds left on the card can be credited back to your client at the end of the budget period.

Advantages of MERPs

Incorporating a MERP into your insurance solution can benefit your client in several ways:

- Maximum spending efficiency: Your client only spends to cover medical expenses their employees incur within their limits. They can enjoy greater predictability and control over their spending than plans with variable costs.

- Flexible plan design: Your client can create their own custom coverage plan for their employees and adjust it yearly. This ensures they can offer exactly the healthcare support that fits their priorities and budget.

- Abundance of data: Implementing a MERP lets your client know exactly how much their employees spend on each type of medical expense using their allowance. This gives them access to a data goldmine for benefit optimization. They can tailor each year's plan based on the previous year's data to maximize the ROI of their benefits budget in employee health, engagement and retention.

- Compatibility with incentives: Your client can combine their MERP with wellness incentives to reward employees for healthy choices. This combo promotes employee health and your client's long-term cost savings. Wellness programs could contribute to a 27% drop in absenteeism, a 25% to 30% drop in healthcare costs for participating employees and an 80% boost in engagement. And 91% of employees participating in wellness programs say they've enhanced their performance.

- Tax-saving potential: MERP contributions and distributions can be tax-exempt for your client and their employees, provided they set up a plan that complies with IRS standards. You can partner with the MERP administrator to guide your client in creating a tax-compliant, money-saving solution for their employees.

- Synergy with other solutions: Your client can pair a MERP with another flexible healthcare benefit and/or a group plan like an HDHP. It's a flexible tool you can incorporate into your healthcare insurance solutions to meet all your client's needs at the best price.

6. Combine Solutions for Maximal Value

While a MERP can be an effective stand-alone healthcare solution for small businesses, MERPs offer added advantages in combination with group plans. Let's explore how pairing a MERP with another healthcare instrument can help you create high-value, low-cost solutions for your clients.

Combining a MERP with an HDHP creates a cost-saving solution often called a Deductible MERP. This hybrid solution secures low premiums for your client through the HDHP while offsetting the employee's contributions through the MERP. Deductibles and co-payments for medical expenses are valid employee uses for the MERP.

For larger clients needing to meet rigorous compliance standards, the HDHP can provide foundational coverage that fulfills regulations. At the same time, the MERP adds flexibility and efficiency. Employees enjoy extra coverage to use as needed, while your client keeps any surplus funds from the reimbursement budget.

You could also create a solution combining a MERP and HSA, potentially on top of an HDHP. The HSA gives your client a tax-advantaged way to contribute to long-term medical savings for their employees. This makes for a benefits package that's attractive to employees while reducing your client's costs.

The Deductible MERP protects the employee's savings for future growth. The savings give the employee a safety net for any larger expenses that may arise. This robust combination will help keep your client's employees healthy, engaged and productive throughout their careers.

Partner With The Difference Card to Create Unbeatable Healthcare Deals

If you're an insurance producer, partner with The Difference Card to optimize your clients' healthcare plan value. Give yourself and your clients a competitive edge with our MERP, HSA and FSA solutions.

The Difference Card equips you to create a custom reimbursement plan aligned with your clients' unique priorities. We can also share our prepackaged suggestions that have produced the best results in our extensive experience. Once your client's plan is set up and initiated, a dedicated account manager from The Difference Card administers every aspect of the plan to streamline your client's experience.

Clients using The Difference Card save an average of over 18% each year on their health insurance costs. When you become an exclusive partner, you stand out from the competition by creating an unbeatable healthcare return on investment for your clients. That's how The Difference Card helped our partners earn an additional $5.1 million in revenue in 2023 alone.

Request a proposal to discover how partnering with The Difference Card can transform your offerings — you'll see the difference.