How to Leverage the Difference Card for Savings

Table of Contents

The Difference Card is a unique platform that guarantees users savings in healthcare spending. In 2023, producer partners achieved $5.1 million in revenue, which equated to $129 million in new medical premiums. What's the secret to how our plans help users save? Read on to learn more about our plan and other cost-saving offerings.

What Is The Difference Card?

The Difference Card is an employer-sponsored benefit that works alongside employees' medical insurance to save costs. Depending on the plan design, users can offset portions of their copays, coinsurance and deductibles with this long-term solution for rising healthcare costs.

The Difference Card works like a credit card — users can swipe to pay for health services in any location that accepts Mastercard, such as doctor's offices, hospitals or pharmacies. It does not show on credit checks, and users will not receive a monthly bill in the mail.

The Difference Card team works with best-in-class brokers to provide custom health benefit solutions, reducing employers' costs while providing quality services. Since its inception, the platform has saved employers an average of 18% off their health insurance spending.

What Tools or Services Does the Difference Card Offer?

The Difference Card uses a Medical Expense Reimbursement Plan. A MERP is an employer-sponsored healthcare plan that reimburses qualified medical expenses, typically offered in conjunction with high-deductible insurance policies.

The employer sets up a plan with rules for eligible expenses and reimbursement. Employees contribute through pretax payroll deductions, which reduce their taxable income. When they incur medical expenses, the employee submits claims and relevant documents to the plan administrator for reimbursement. As the plan administrator, The Difference Card reviews the claim to ensure it meets the criteria.

A MERP plan usually covers various medical expenses:

- Doctor visits

- Medical prescriptions

- Surgical treatment

- Hospitalization

- Emergency or urgent care visits

- Vision prescription

- Physical therapy

Employers can design a MERP plan according to their business needs and administrative capacities. Moreover, they must comply with regulations like the Employee Retirement Income Security Act and the Internal Revenue Code. The Difference Card provides complimentary compliance services to help clients conform to regulatory standards.

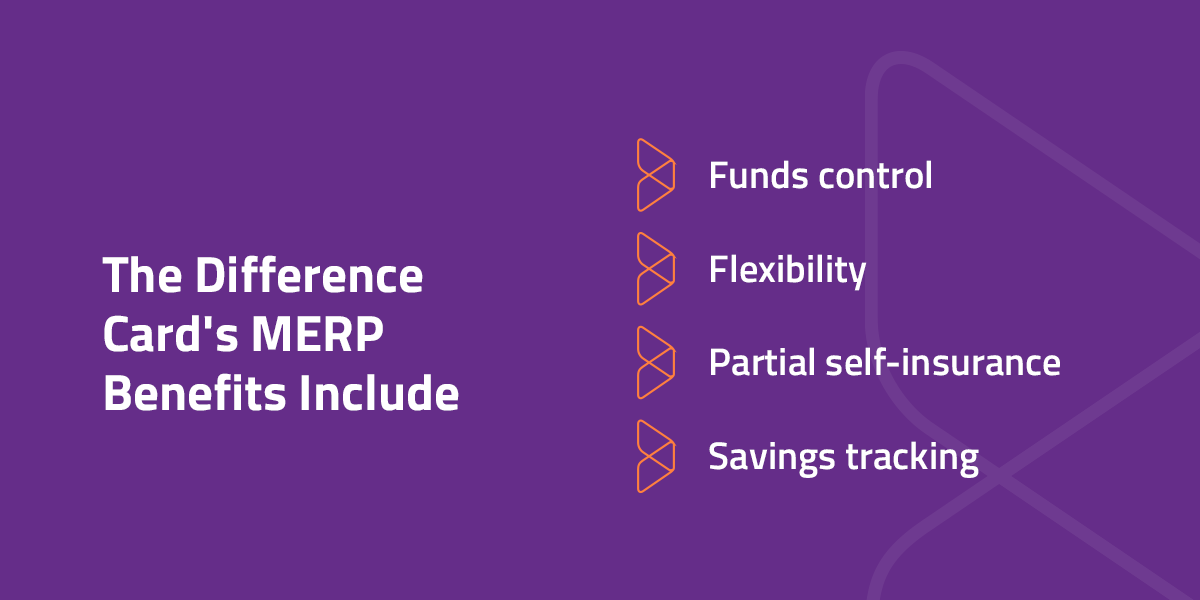

The Difference Card's MERP benefits include the following.

- Funds control: Employers, instead of carriers, retain unspent funds at the end of the year.

- Flexibility: Employers can switch carriers and adjust plan designs while maintaining the MERP benefits.

- Partial self-insurance: A MERP plan allows employees to self-fund part of their medical benefits, saving employers associated costs.

- Savings tracking: The Difference Card tracks savings, providing users with tangible metrics.

How to Use These Tools for Savings

In addition to the MERP product, The Difference Card provides offerings employers and employees can use to increase savings.

1. Health Savings Account

An HSA is a personal savings account that allows employees to set aside pretax dollars for qualified health costs for themselves and their dependents. Employees can also make direct contributions, but the pretax payroll deduction reduces taxable income and out-of-pocket costs by letting people use untaxed savings to pay copayments, coinsurance, deductibles and other expenses. Employers can contribute to the account and deduct the amount from their tax liability — an excellent way to save for retirement.

Employers must select a compatible qualified high-deductible health plan with lower premiums and higher deductibles than traditional health insurance plans. Employees must enroll in the HDHP and cannot have other non-HDHP coverage like Medicare. The money in an HSA can grow tax-free through earnings such as investments and interests. Withdrawals for qualified medical expenses are also tax-free.

2. Flexible Spending Account

An FSA is a tax-advantaged financial account that allows employees to set aside portions of their pretax salaries to cover eligible medical expenses for themselves and their dependents. FSA contributions reduce employees' taxable income and potentially lead to tax savings. Funds can cover costs like copayments, coinsurance and deductibles. The distinguishing feature is that people enrolled in an FSA must generally spend unused funds within the plan year or risk losing them, though some plans provide grace periods or a roll-over feature.

The difference between an HSA and an FSA is that an HSA belongs to the employee, whereas an FSA belongs to the employer. Also, an HSA requires a qualified HDHP, but an FSA does not. All employees are eligible for an FSA regardless of their insurance status. A self-employed person can participate in an HSA but not an FSA.

3. Health Reimbursement Arrangement

An HRA is an employer-sponsored reimbursement account that allows employees to pay eligible healthcare expenses. Unlike other accounts for which the IRS determines the eligible services, an HRA allows employers to define the reimbursement services. Employers can choose the covered healthcare service and provide tailored benefits, reducing their employees' financial burden.

An HRA also offers tax advantages. Employers solely fund these accounts and can deduct the expenses when filing their tax returns. With an HRA, unused funds do not usually roll over to the following year, though some employers offer carryover provisions.

There are four different types of HRA:

- Integrated: This HRA aligns with group health insurance plans, often alongside an HDHP.

- Individual: This arrangement allows employees to use HRA funds to buy individual health insurance.

- Expected benefit: This type of HRA offers limited benefits for vision, dental and other expenses regardless of other health coverage.

- Qualified small employer: An HRA designed for small businesses, usually those with fewer than 50 employees.

The Difference Card brings value to users. In addition to the benefits discussed above, we provide a myriad of cost-saving offerings, including dependent care accounts, lifestyle spending accounts and incentive-based wellness programs. These solutions enable users to reduce health insurance costs while maintaining quality benefits.

Choose The Difference Card for Healthcare Savings

The Difference Card has provided customized, affordable healthcare solutions for over 20 years. We work to understand our partners' needs and help them reduce their tax and financial burdens. We provide guaranteed savings solutions by letting employers tailor benefits and limit claim exposure while insured by an A-rated carrier.

The Difference Card team values customer relationships. We dedicate time to addressing client needs and make ourselves readily available. Our professionals are trustworthy and responsive, so you can be confident you are in good hands. Request a proposal today to learn more!