What Is a Hybrid Approach for HDHPs?

Table of Contents

- Key Differences Between a Hybrid HDHP and Traditional HDHP

- The Benefits of a Hybrid Healthcare Plan

- Creating a Hybrid HDHP for Employees

- Common Misconceptions About an HDHP

- FAQs About a Hybrid HDHP

- How Does The Difference Card Help Brokers and Companies?

- Get The Difference Card for Cost-Effective Healthcare Solutions

A hybrid High Deductible Health Plan (HDHP) is typically paired with a Health Reimbursement Arrangement (HRA) or a Health Savings Account (HSA). It offers cost-saving and tax advantage benefits that can make healthcare more accessible to a broader demographic than traditional healthcare plans or a straight HDHP.

What Is a Hybrid High Deductible Health Plan?

An HDHP has a larger annual deductible than a traditional health plan. In exchange for this larger deductible for medical expenses, it has lower monthly premiums, making it a sought-after alternative to the usual options.

The Internal Revenue Service (IRS) lists an HDHP as having an annual deductible of at least $1,600 for individual coverage and $3,200 for family coverage. The yearly out-of-pocket expenses for an HDHP — excluding premiums — shouldn't exceed $8,050 for individuals or $16,100 for families.

HDHP plans offer complete coverage for routine preventive care without the need for coinsurance or copays if the deductible hasn't been met. Here are a few services that fall under this coverage:

- HIV screening

- Diet counseling

- Depression screening

- Blood pressure screening

- Immunizations for diseases like measles, chickenpox and the flu

A hybrid HDHP combines another type of plan, usually an HSA or HRA. Pairing it with an HSA is the more popular option because it offers recipients a tax-advantaged account that includes tax-free deposits, interest growth and withdrawals for qualifying expenses.

A hybrid HDHP still involves a deductible, which the recipient pays initially for all medical care. Then, there's a copay for specific medical care, like doctor's visits. These plans are designed to meet an individual's or family's needs.

Healthcare plans are legally required for organizations with 50 or more full-time employees. So, it's vital to choose an option that complements both parties. Employers and employees can contribute to a hybrid HDHP paired with an HSA so they face minimal risk and maximum returns. A hybrid HDHP contains copays, but it's also protected by the out-of-pocket maximum, which makes it a top pick for many.

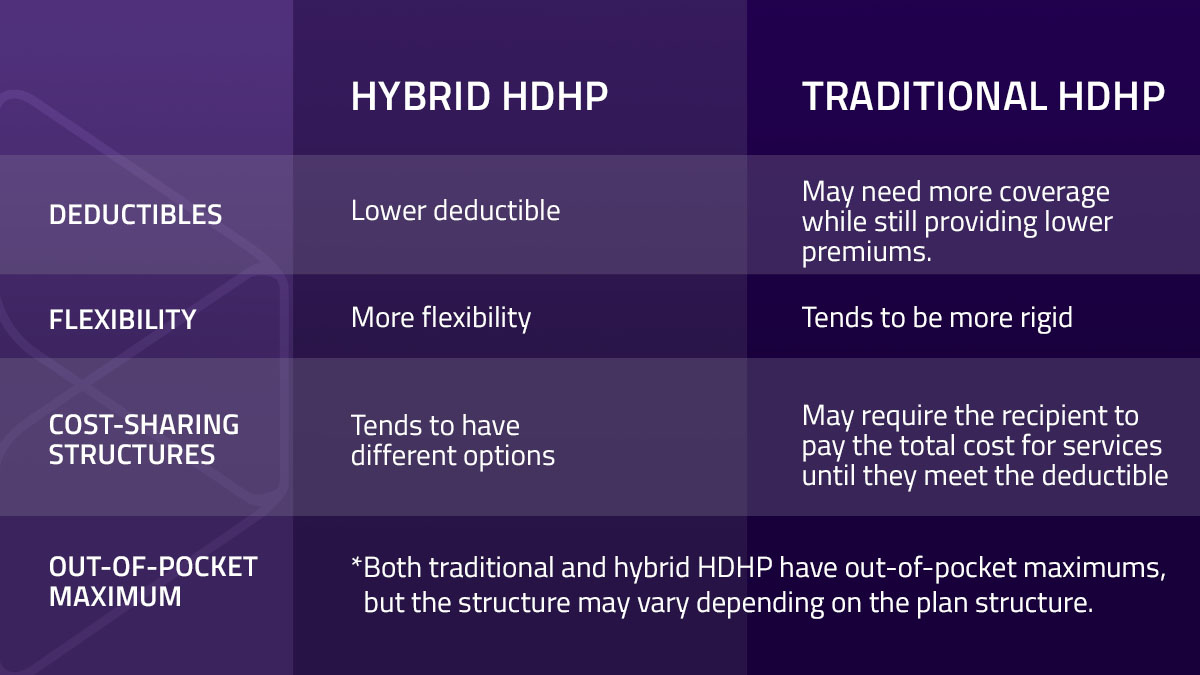

Key Differences Between a Hybrid HDHP and Traditional HDHP

A hybrid HDHP and a traditional HDHP have unique differences that can make one or the other stand out depending on the individual's needs. Here are the key differences between the two:

- Deductibles: A hybrid HDHP tends to have a lower deductible than a traditional HDHP. Hybrids can offer close to the high deductible of a traditional HDHP for areas where the individual may need more coverage while still providing lower premiums.

- Flexibility: A hybrid HDHP offers more flexibility than a traditional HDHP, which tends to be more rigid. Hybrids show their flexibility when recipients get coverage for some services before they meet the deductible.

- Cost-sharing structures: A traditional HDHP may require the recipient to pay the total cost for services until they meet the deductible, while a hybrid HDHP tends to have different options, like copayments, that the recipient can use to pay for services before meeting the deductible.

- Out-of-pocket maximum: Both traditional and hybrid HDHP have out-of-pocket maximums, but the structure of hybrid options may vary depending on the plan structure.

The Benefits of a Hybrid Healthcare Plan

A hybrid HDHP has various benefits like enhanced cost-efficiency, improved accessibility and better continuity of care. An HDHP has multiple advantages over traditional healthcare plans, especially for people who don't get sick as often. Here are the top benefits of a hybrid health insurance plan:

- Cost efficiency for providers and patients: A hybrid HDHP provides a more cost-effective option for recipients. Individuals can use copayment options even before meeting the deductibles, allowing them to save on out-of-pocket costs.

- Enhanced continuity of care: A hybrid HDHP may focus more on continuity of care, which is crucial for patient engagement and quick recovery. Hybrid models may offer them a wider range of channels for contacting their healthcare providers. They might receive more resources and communication tools, which could be pivotal to their recovery and help fill gaps in healthcare.

- Lower monthly premiums: A hybrid HDHP delivers monthly coverage for lower premiums, which is an attractive perk for both employers and employees.

- Reduced medical expenses: Individuals who don't need frequent healthcare may spend less on their monthly insurance payments.

- Improved patient accessibility: A hybrid HDHP offers patients more accessible options. Improved accessibility is especially useful for patients with time constraints, transportation issues or mobility difficulties.

- Increased savings: Since an HDHP is the only healthcare plan that pairs with an HSA, it's ideal for individuals who wish to use pretax funds for possible health expenses. Additionally, the savings that individuals collect are theirs to keep, and they can even hold on to the HSA if they decide to close their HDHP.

Creating a Hybrid HDHP for Employees

Brokers can help employers customize health plans that are better suited to their employees' needs. Here are the typical steps involved in creating a hybrid HDHP:

1. Consider the Demographic Needs

Employee demographics may form the foundation for the health concerns they typically face. Employees who have children may be interested in maternal and birth care benefits or adding benefits. Younger, single employees like millennials and Gen Z may care more about preventive care and lower premiums, with care focused on conditions like migraines and obesity.

Companies should survey their employees on their healthcare preferences to attain direct insights and work with an experienced broker to offer employees a hybrid HDHP that works for them.

2. Decide on the Plan's Goals

A successful hybrid HDHP must align with the business's strategic goals. Choosing a hybrid health insurance plan that suits employees' goals can offer the following benefits:

- Increases morale: Competitive coverage can make employees feel more valued and satisfied, which leads to increased morale and productivity.

- Improves employee health: Offering healthcare plans catered to the employees' preferences can help reduce absenteeism and enhance focus and effort.

- Saves costs: Instead of choosing a traditional plan that covers everything, an HDHP catered to employees' demographics and needs can help companies choose more streamlined and cost-effective plans.

3. Reach a Realistic Budget

Healthcare costs rise over time, and it can be challenging for companies to keep up with premiums if they don't start on realistic terms. Businesses must establish a clear budget and find the best ways to allocate costs. Here are some of the popular strategies they may employ:

- HSA or Flexible Spending Account (FSA): These account types help companies offer a more comprehensive option while assisting employees with a medical expense saving account for pretax funds to cover out-of-pocket expenses.

- Cost-sharing: Companies and their employees can both contribute toward premiums. To make this option more suitable for different demographics, businesses can offer different premium ranges so employees can select the cost and coverage they prefer.

- Incentives and wellness programs: Companies can create wellness programs and offer incentives, such as gym memberships or step-count rewards, to lower healthcare costs in the long run.

4. Offer a Selection of Coverage Options

Companies offering a flexible hybrid HDHP allow employees to choose the most beneficial plan. Here are the factors to consider when building a group insurance package:

- Health plan types: Companies should aim to offer various hybrid health insurance types to cater to different demographics and health plan preferences.

- Dental and vision add-ons: Some employees may prefer to add these options for a more comprehensive package.

- Life and disability insurance: Options like accidental death and dismemberment can help employees make decisions to secure their financial futures and their family's stability.

- Supplemental options: Some employees may want to add emergency financial support like hospital indemnity insurance.

5. Cooperate With an Experienced Broker

Selecting the right broker can help companies design a hybrid HDHP that aligns with their and their employees' needs. An experienced professional can help businesses negotiate better rates and tailor their coverage options to their requirements and worker demographics.

Partnering with financial professionals who go the extra mile to craft the best deals for the employees and the company can make all the difference in health plan options. Look for other ways to support your employees, like maximizing reimbursements, to give them a positive experience and make them feel valued.

6. Educate Employees on Hybrid HDHP Options

Employees must understand the insurance plan options and how to use a hybrid HDHP to their benefit. Resources like webinars or even one-on-one consultations can help them understand their options and make informed choices. Here are some of the topics that educational resources should cover:

- Cost-sharing options: Include information on how much the company is willing to subsidize for different plans. For example, employers may match an employee's HSA contributions, which would be a significant perk to help businesses develop competitive packages.

- Differences between plans: Outline the different hybrid HDHP options and provide the pros and cons for each one.

- In-network providers: Highlight the benefits of using in-network providers for more accessible and cost-effective care.

7. Review Regularly

The company's needs, employee demographic and vision will change over time. Collecting feedback is the best way to retain clients and improve services. Regularly review these factors with key metrics like employee feedback and plan participation rates.

Yearly scheduled reviews work for most companies and can help brokers discover areas for improvement.

Common Misconceptions About an HDHP

When pitching an HDHP to employees, there may be some confusion or even disappointment due to common myths surrounding this plan. Brokers should provide knowledge and educational resources to break these myths.

Here are the two major myths surrounding HDHP options:

Myth 1: A High Deductible Health Plan Will Cost Too Much

A traditional HDHP may not be the best solution for an individual who requires many doctor visits, but a hybrid HDHP could be. For example, a hybrid HPHD with an HSA can offer tax advantages and lower premiums.

Many believe that HDHP options will cost too much because of the higher deductible but forget that a hybrid HDHP usually has significantly lower premiums. So, even if an individual has multiple healthcare expenses, they can save money by choosing a hybrid HDHP.

Some employers may even reward employees for choosing an HDHP with contributions toward an HSA.

Of course, suppose an individual has a chronic condition requiring consistent doctor visits and specialized care. In that case, they must decide whether the savings from lower premiums are greater than the out-of-pocket costs for regular healthcare checks.

Myth 2: An HDHP Is Only for Young People

While an HDHP is typically recommended for younger demographics, an HDHP hybrid may be more beneficial for healthier, older people. Combined with an HSA, an HDHP option can boost retirement savings.

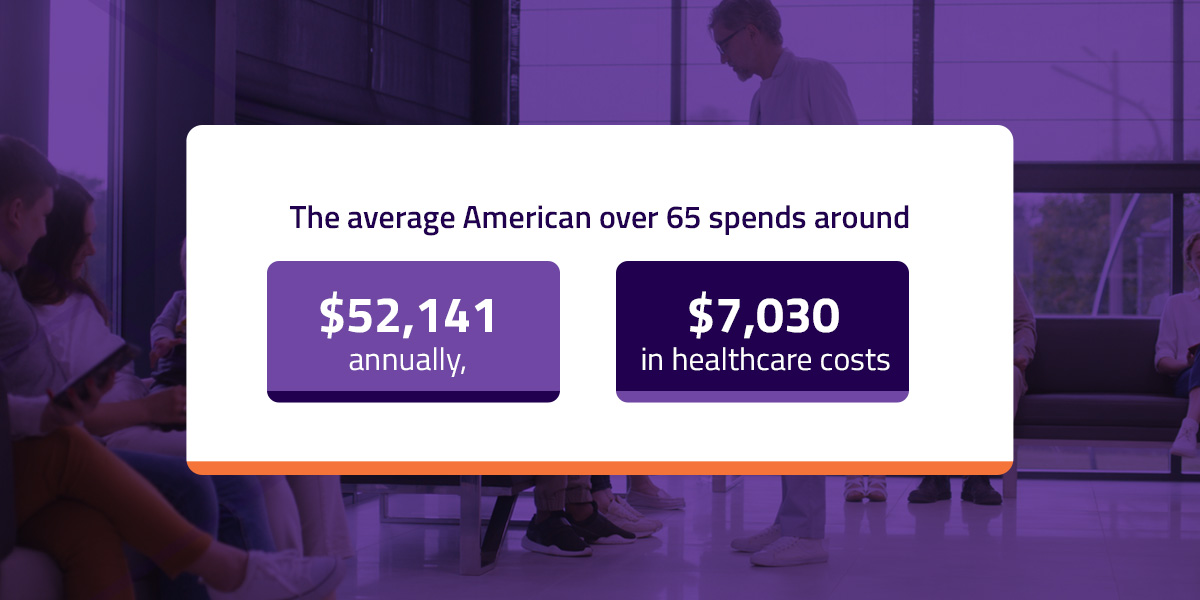

The average American over 65 spends around $52,141 annually, and around $7,030 is healthcare costs. An HSA, especially one that an employer subsidizes, is an excellent way for older employees to save for healthcare expenses during retirement.

A hybrid HDHP can offer older demographics peace of mind and a way to prepare for the future.

FAQs About a Hybrid HDHP

A hybrid HDHP may seem complicated, but these answers to the most commonly asked questions about an HDHP can clear things up:

How Does a Hybrid Plan Improve Healthcare Benefits?

Hybrid plans improve healthcare benefits by giving individuals a set of features, such as premiums and deductibles, that suit their preferences.

Is a Hybrid HDHP Suitable for All Employee Demographics?

A hybrid HDHP is suitable for most demographics. It may not be the best option for individuals with chronic conditions that require frequent and consistent medical care.

What Are the First Steps to Implementing a Hybrid HDHP?

The first steps for companies wanting to implement a hybrid HDHP are to consider the demographic and decide on the goals and budget.

How Does The Difference Card Help Brokers and Companies?

The Difference Card is a one-of-a-kind platform that allows companies to save on healthcare without compromising on quality offerings. Brokers can use it to save employers money and help employees get medical insurance that suits their needs. In 2023, producer partners who used The Difference Card hit $5.1 million in revenue with $129 million in new premiums.

The Difference Card can save businesses over 18% annually and protect them from unnecessary risks. Here are some of the products companies can enjoy with The Difference Card:

- Medical expense reimbursement plans (MERP): They save companies 18% of fees by setting up partially self-funded structures that incorporate multi-line benefits like hospitalization, urgent care and dental.

- HSA: It provides triple-tax advantaged accounts with impressive investment possibilities.

- FSA: This employee-funded account enables staff to pay for their healthcare expenses with pretax funds.

- HRA: This arrangement sets up employer-funded accounts, allowing recipients to access funds for healthcare costs at a fixed annual amount.

Get The Difference Card for Cost-Effective Healthcare Solutions

The Difference Card has been providing healthcare solutions for over 20 years, saving its clients up to $1 billion and counting. In addition, we hold a client satisfaction ranking within the top 100th percentile in the insurance and health category.

If you want to streamline your healthcare plan, there's no better option than The Difference Card. Request a proposal from us today and start saving money on your healthcare plan.