Insurance Cost Management for Brokers

Table of Contents

- What Is Insurance Cost Management?

- Benefits of Insurance Cost Management

- Role of Brokers in Insurance Cost Management

- Factors Influencing Insurance Costs

- Cost-Saving Strategies for Brokers

- Effective Risk Management for Cost Control

- Enhancing Broker-Client Relationships

- Navigating Insurance and Risk Management Trends

- Save Health Insurance Costs With The Different Card

If you're a broker, reducing costs like insurance premiums and deductibles can help you provide value to clients. Fortunately, you can achieve that through insurance cost management. This guide discusses the concept, including the benefits and the role of brokers. You will also learn common strategies, best practices and how The Difference Card helps.

What Is Insurance Cost Management?

Insurance cost management involves analyzing, planning and implementing measures to optimize insurance expenditures. In other words, it is the technique used to control expenses associated with insurance premiums, claims and related costs. The goal is to maximize the value derived from insurance coverage while minimizing financial burdens.

Insurance cost management covers the following areas:

- Risk assessment and mitigation: This component is the foundation of cost management. It involves identifying potential risks, assessing potential impact and implementing strategies to reduce risks.

- Claims management: This component involves strategies like prompt incident reporting and accurate documentation. Implementing systems to prevent claims through proactive measures is also crucial.

- Negotiation and procurement: These typically involve comparing quotes and negotiating contracts. Brokers must understand clients' needs and industry trends to find the ideal coverage.

- Data analysis and reporting: Another crucial aspect is analyzing insurance data, including claims history and premium costs. It helps pinpoint areas of improvement and track the effectiveness of cost-management strategies.

- Employer and employee education: Educating employers and employees about risk management and promoting safe practices can significantly reduce the frequency and severity of incidents leading to claims.

- Technology and automation: Technology like claims management software and risk assessment tools can streamline processes, improve efficiency and reduce administrative costs.

Benefits of Insurance Cost Management

By implementing cost management strategies, individuals and organizations can reap many benefits. Here are some examples:

1. Reduced Premiums

Insurance cost management can lower premiums by removing unnecessary expenses. It ensures clients are not overpaying for coverage. Brokers can help clients obtain multiple quotes, allowing them to choose the most cost-effective option.

2. Improved Cash Flow

Lower insurance costs translate to better cash flow, giving businesses and individuals more flexibility in allocating resources to other strategic initiatives or investments. Insurance cost management also helps clients predict expenses more accurately, which can aid budgeting and financial planning.

3. Enhanced Insurance Risk Management

A key component of insurance cost management is assessing and mitigating risks. By implementing safety measures and best practices, clients can reduce the likelihood of claims and associated costs. Saving clients money can build trust and long-standing relationships.

4. Increased Profitability

Reduced insurance expenses can directly contribute to higher profit margins and overall profitability. Businesses can reinvest savings from insurance costs to support growth and innovation.

5. Access to Better Coverage

Clients can secure the most appropriate coverage tailored to their specific needs through cost management without overspending. Companies can afford to purchase more comprehensive policies or additional coverage options that might have been financially impractical without cost management.

6. Improved Claims Experience

Insurance cost management often includes claims advocacy, which facilitates claims filing and can reduce the administrative burden on clients. Brokers can assist with claims processing and negotiation, ensuring clients receive fair compensation promptly.

7. Employee Benefits Enhancement

For organizations offering employee benefits, cost management can improve health insurance plans and other benefits without significantly increasing costs. Competitive benefits can also attract and retain top talent, contributing to organizational success.

8. Long-Term Financial Stability

By integrating insurance cost management into financial strategy, clients can build a sustainable approach to managing risks and costs over the long term. It prepares clients better to handle fluctuations in the insurance market and economic conditions.

9. Data-Driven Decision-Making

Regularly analyzing insurance data and claims history allows clients to make informed decisions about their coverage and risk management strategies. Ongoing monitoring and reporting enable clients to identify trends, assess the effectiveness of cost management strategies and make necessary adjustments.

Role of Brokers in Insurance Cost Management

Insurance brokers act as intermediaries between clients and insurance providers. They use their industry experience to help clients navigate insurance complexities and secure suitable coverage. Here is an overview of the role of brokers in insurance cost management:

1. Market Knowledge and Access

Brokers have insight into the insurance market, including various insurers, their products and pricing structures. With this knowledge, they help clients find the best coverage options at competitive prices. Insurance brokers can access multiple insurers and provide clients with quotes and terms to compare.

2. Tailored Insurance Solution

Brokers work to develop customized insurance solutions that address unique client needs. By tailoring coverage, clients pay only the necessary coverage while getting adequate protection against potential risks.

3. Risk Assessment and Placement

Brokers conduct thorough risk assessments to understand clients' needs and risk exposures. This assessment enables them to recommend appropriate coverage levels and types. By placing clients with the right insurers that offer competitive rates for their risk profiles, brokers help control premium costs.

4. Negotiation

Brokers can help clients during the insurance procurement process. They can negotiate terms, coverage limits and pricing to save clients money. Moreover, brokers can leverage their relationships with underwriters to find practical solutions when challenges arise.

5. Claims Advocacy

In the event of a claim, brokers can advocate and ensure claims are handled efficiently and fairly. A positive claims experience can influence future insurance costs, as it can minimize the impact of claims history on premium pricing. Also, by providing support during the claims process, brokers can help clients avoid pitfalls that can potentially increase costs and deny claims.

6. Ongoing Policy Review

Brokers can regularly review clients' insurance needs and policies. This proactive approach allows them to identify opportunities for cost savings, such as adjusting coverage as business needs change or eliminating unnecessary policies. Brokers can also alert clients of changes in the market or regulations that may affect their insurance costs.

7. Client Education

Brokers usually educate clients about their insurance options, features and the implications of different coverage levels. This knowledge helps clients make informed decisions that align with their financial goals and risk tolerance.

8. Long-Term Relationship Management

Brokers can build long-term client relationships, fostering trust and ongoing communication. This relationship enables brokers to stay in tune with clients' evolving needs. It allows for timely adjustments to insurance coverage and cost management strategies.

9. Monitoring and Reporting

Brokers monitor clients' insurance policies and claims experience over time. They may provide regular reports and insights on insurance costs and claims history, helping clients understand their risk profile and how it affects their premiums.

Factors Influencing Insurance Costs

Internal and external factors impact the cost of health insurance. As a broker, you must understand these considerations to guide clients in finding the ideal coverage. Here's an overview:

Internal Factors

Internal factors relate directly to the prospective policyholder. Examples include:

- Employee demographics: The average age and gender distribution of employees can impact health insurance costs, and the health of the employee population is also crucial.

- Plan design and coverage options: The health insurance plan directly impacts costs. Employee contributions, deductibles, copayments and out-of-pocket maximums are vital considerations.

- Employee utilization of health care services: If employees file more claims, costs can increase. Employers encouraging preventive care can reduce costs in the long run by avoiding severe health issues.

- Wellness programs and initiatives: Employers that invest in wellness programs can reduce health insurance costs over time. These initiatives can reduce claims and improve employee health.

- Claims management: Efficient claims management can decrease administrative costs. Employers can also control costs by negotiating rates or using third-party administrators to manage claims.

External Factors

External factors are outside the control of the prospective policyholder. Examples include:

- Economic conditions: Rising health care costs due to inflation can increase insurance premiums. Low interest rates can impact insurers' investment income, prompting them to increase premiums.

- Regulatory environment: Changes in health care laws, such as the Affordable Care Act (ACA), can impact employer-sponsored health insurance costs. State legislation regarding minimum coverage requirements is also a critical consideration.

- Market competition: The level of competition among health insurance providers can influence premiums. In highly competitive markets, insurers may offer lower rates to attract employers.

- Technological advancements: Introducing new technologies and treatments can determine health care and premium costs. Telehealth services are a classic example.

- Social trends: Changing employee expectations can influence costs. For instance, employers may need to enhance benefits to attract and retain talent.

- Public health emergencies: Health emergencies like pandemics can strain health care resources, potentially increasing insurance costs. The rise of chronic diseases is another example.

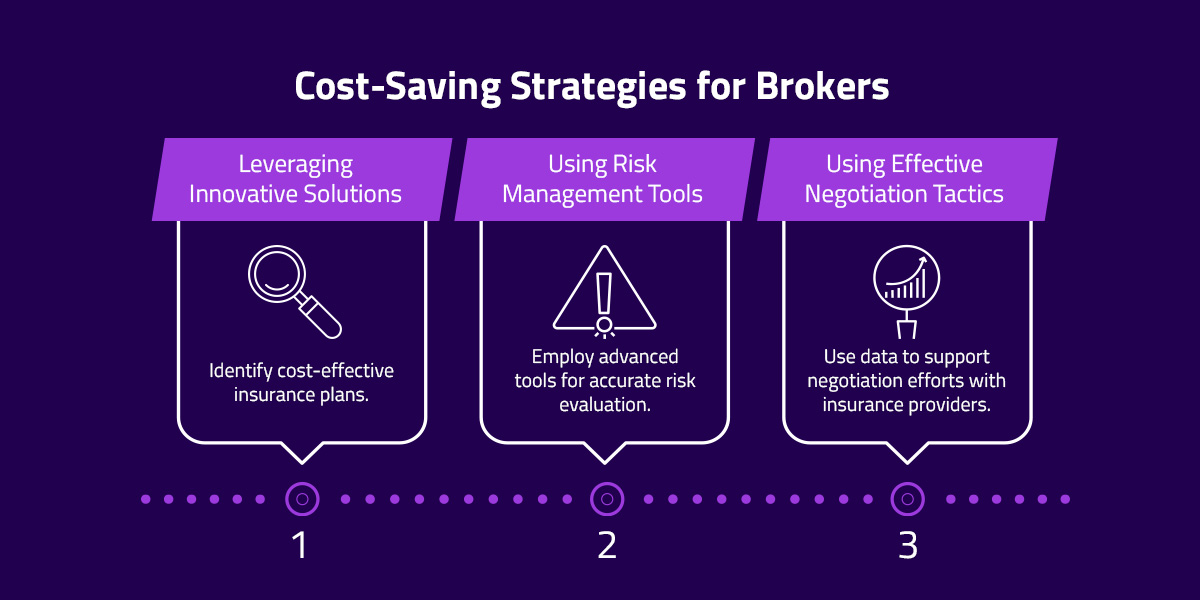

Cost-Saving Strategies for Brokers

There are several ways to reduce health insurance costs for clients. These include:

1. Leveraging Innovative Solutions

First, identify cost-effective insurance plans. You can achieve this through comprehensive market analysis, customized solutions and alternative funding arrangements. Second, leverage The Difference Card's proprietary solutions. As a broker, you can use the platform to help employers manage their health care costs better.

2. Using Risk Management Tools

Employ advanced tools for accurate risk evaluation. An example is predictive analytics software, which you can use to assess clients' risk profiles. Additionally, you can promote telehealth services as a convenient solution for accessing health care. Telehealth can reduce unnecessary emergency room visits and lower costs.

3. Using Effective Negotiation Tactics

Use data to support negotiation efforts with insurance providers. Presenting compelling data can help you find favorable terms and lower client premiums. When negotiating for multiple clients or large groups, you may bundle them together to get competitive rates or improved benefits. Furthermore, build strategic collaborations with insurance providers. This relationship can facilitate negotiations.

Effective Risk Management for Cost Control

Effective risk management can help control health care insurance costs. But how do you achieve that? Here are some helpful tips:

1. Implementing Risk Management Techniques

There are three primary components of risk management:

- Identification: The first phase of risk management involves identifying potential risks associated with health care insurance. These could be financial, operational or compliance risks. Collaborate with health care providers, insurers and employers to gather insights.

- Assessment: The second phase involves evaluating the risks you have identified. You can use quantitative or qualitative methods to prioritize them. You can also compare risk profiles against industry benchmarks to identify areas for improvement.

- Mitigation: Finally, implement mitigation strategies. These may include executing preventive measures, choosing insurance options according to client needs or guiding clients through the contract stage.

2. Employing Technology

Automating functions like risk reporting can streamline processes and reduce manual errors. Also, implement solutions that enable real-time monitoring of health care trends to enable quick adjustments.

Enhancing Broker-Client Relationships

Transparent communication is an excellent strategy for building trust with clients. When brokers openly communicate policies, coverage options, costs and potential risks, clients feel confident in their decisions. Clear communication helps manage expectations and reduces misunderstandings. Again, keeping clients informed about developments like changes in regulations and insurance products demonstrates your commitment to your clients' best interests.

It is essential to engage clients regularly to discuss their needs and concerns. You can leverage their feedback to gauge sanctification. You can develop personalized solutions to address gaps based on the information you gather. Finally, position yourself as an industry expert by sharing insights, trends and best practices. This builds credibility and reassures clients that they are in capable hands.

Navigating Insurance and Risk Management Trends

Health insurance brokers must understand industry trends and adapt to stay relevant. It's essential to pay attention to the following areas:

- Digital transformation: Technology is empowering health insurance brokers worldwide. A classic example is customer relationship management (CRM) software to improve customer services. These innovations are diverse and can help you achieve your goals.

- Client-centric approaches: Brokers are investing in customer engagement initiatives to provide excellent services. As expectations increase industry-wide, catering to clients' needs has become even more important. One such expectation is affordable, quality health care.

- Regulatory changes: The insurance industry is adapting to evolving regulations, such as data privacy laws and health care mandates. Additionally, the shift to remote work has changed the dynamics of risk management. Insurers and brokers are adjusting their offerings to address these new challenges.

Save Health Insurance Costs With The Different Card

Are you ready to help your clients reduce insurance costs? Look no further. The Difference Card is the ideal platform.

We work with brokers to create custom health benefit plans for employers, allowing them to save an average of 18% on their health insurance spending. Our partnership with the best-in-class brokerage agencies and independent agents nationwide has helped grow their businesses.

The Difference Card delivers innovative health insurance solutions to reduce employer health insurance costs while providing quality coverage to employees. Want to learn more? Contact us now!