How to reduce healthcare costs with a MERP

Table of Contents

Many families worry whenever they have to deal with medical conditions and associated medical expenses. In 2023, the annual medical cost for a family of four in the U.S. was $31,065. To provide relief from medical expenses, employers offer various forms of healthcare plans or benefits for their employees.

In addition to the traditional group health insurance, employers can simply reimburse their employees for the medical costs incurred. Through health reimbursement arrangements (HRAs), you as an employer can only incur expenses when reimbursing employees for medical costs. For an employee, you get compensated or reimbursed for the money you've spent on treatment. One of these arrangements is medical expense reimbursement plans (MERPs).

Understanding MERP Basics

A MERP is a health reimbursement arrangement between an employee and an employer in which the employer covers some of the employee's healthcare costs. The employer reimburses workers for out-of-pocket medical expenses and individual health insurance premiums. The goal of a MERP is to provide employees with relief from the burden of medical expenses.

MERPs are recognized under Section 105 of the Internal Revenue Code (IRC) and create tax-free funds for employees to pay their health plan deductibles, co-payments, co-insurance and other qualified medical expenses. The workers or their dependents may incur these expenses. The employer reimburses the employee for incurred medical expenses. This approach is adaptable and responsive to each worker's healthcare needs.

What MERPs Cover

MERPs allow employers to set annual reimbursement limits for every employee. The limit is the highest amount the company or organization will reimburse the employee for qualified medical expenses in a given year. To be eligible for reimbursement, the medical expense must be approved under the group health plan guidelines.

Common MERP-eligible expenses include:

- Acupuncture

- Asthma inhalers

- Blood pressure monitors

- Chiropractic care

- Co-pays

- Dental expenses

- Face masks

- First aid supplies

- Glasses, contact lens solution and contact lenses

- Glucose monitors

- Hospital care

- Health insurance premiums

- LASIK

- Many fertility procedures

- Menstrual care products

- Over-the-counter medicines

- Prescription medications

- Sunscreen

How MERPs Work for Employers

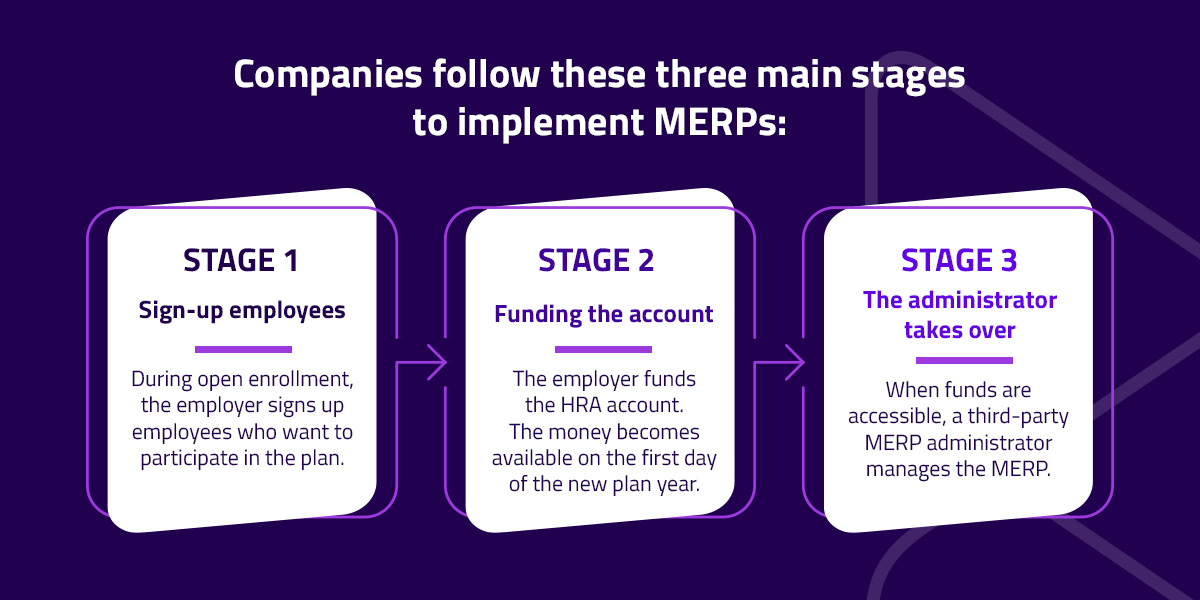

Companies follow these three main stages to implement MERPs :

- Sign-up employees: During open enrollment, the employer signs up employees who want to participate in the plan.

- Funding the account: The employer funds the HRA account. The money becomes available on the first day of the new plan year.

- The administrator takes over: When funds are accessible, a third-party MERP administrator manages the MERP.

MERPs generally follow a five-stage process for reimbursement of medical expenses:

- The employer sets a limit for each employee: The employer defines the allowances for each employee and sets the annual limit. The employer can set different allowances for different employees based on factors such as family size, employee status or job-specific roles.

- Employees purchase healthcare services or products: Specific rules and offerings determine what they can spend their money on and get reimbursement. Employees are not confined to a network and can choose services or providers that best meet their individual or family health needs.

- Employees submit proof of expense: To claim reimbursement from the employer, employees must submit proof of medical expenses, such as invoices, receipts and statements from healthcare providers. These documents must show the date the medical services were provided, the services provided and the expenses incurred.

- The employer reviews the documentation: This process verifies the costs are eligible under applicable terms and that the company spends money only on legitimate claims. It also ensures expenses are within the set limit for that specific period.

- The employer reimburses employees for verified medical expenses: The reimbursement is typically made through payroll and is tax-free for employees.

Key Features of MERPs

The main features and benefits of MERPs include the following:

- Flexibility: Employees can use the funds to pay for various medical costs not covered by the health plan, including co-payments, deductibles, co-insurance, prescriptions, vision care and dental care.

- Freedom: The employer can set up or change insurance plans without changing the MERP administrator.

- Tax savings: Reimbursements for employees' medical expenses are tax-exempt, and employer contributions are tax-deductible expenses.

- Control: The employer decides the amount of money available to employees and how it will be disbursed. There is no carrier intervention to direct the employer on what they can and cannot do. The employer designs cost-sharing and employee responsibilities.

Strategies to Reduce Healthcare Costs

Adopting a MERP for your organization or business can significantly reduce healthcare costs.

How MERPs Reduce Healthcare Expenses

MERPs allow employers to set an annual limit for each employee. The company is not liable to pay for medical expenses exceeding the set limit for that specific year. These limits and the predictability of total annual costs allow companies to budget for employees' healthcare based on the available resources. The employer's ability to set limits ensures control of healthcare spending.

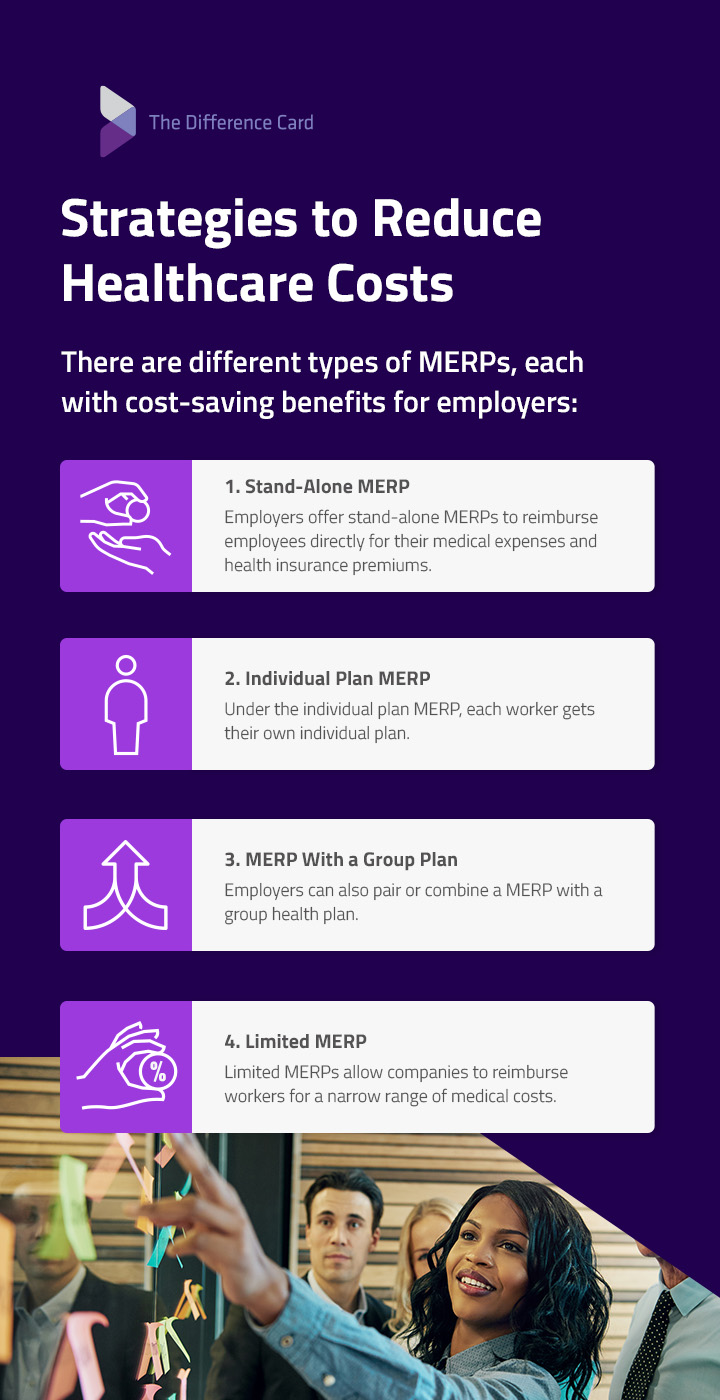

There are different types of MERPs, each with cost-saving benefits for employers.

1. Stand-Alone MERP

Employers offer stand-alone MERPs to reimburse employees directly for their medical expenses and health insurance premiums. Instead of providing a group plan, the employer gives each worker an allowance to purchase their own coverage. Stand-alone MERPs give companies flexibility and control over costs compared to traditional group plans. Premiums for traditional group plans rise sharply year after year.

An example of stand-alone MERP is a qualified small employer HRA (QSEHRA), which the federal government designed for businesses with fewer than 50 full-time employees. QSEHRA allows companies to set aside a fixed amount each month for employees to spend on medical services or purchase individual health insurance. This option relieves the employer of the hassle of administering the traditional group plan while allowing the employer to enjoy tax benefits.

2. Individual Plan MERP

Under the individual plan MERP, each worker gets their own individual plan. This type of MERP is called an Individual Coverage Health Reimbursement Arrangement (ICHRA). The company sets up an ICHRA for every employee. This plan can function as a stand-alone benefit or a separate option in a company's health benefits program.

The employer can offer one class of employees a health insurance plan and provide ICHRA to another class of employees. For example, the company may offer ICHRA to part-time employees and a group health insurance plan to full-time employees. These options are also cost-effective and convenient when some employees are in locations not well-served by traditional group plans.

3. MERP With a Group Plan

Employers can also pair or combine a MERP with a group health plan. The most preferred plan is a high-deductible health plan (HDHP), which allows employers to raise the deductible on the existing health plan and reimburse workers for the difference. This strategy leads to significant MERP insurance savings for the company without any change in coverage.

MERPs paired with group plans are commonly called integrated HRAs, deductible HRAs, group HRAs or traditional HRAs. No matter the label, the goal is to lessen the burden of higher deductibles for the employees.

4. Limited MERP

Some companies offer a tailored MERP that reimburses employees only for designed medical expenses. Limited MERPs allow companies to reimburse workers for a narrow range of medical costs. For example, the organization may decide to cover only dental and vision costs. In such cases, employees can claim reimbursements for glasses, eye exams, dental cleaning or other dental services. They won't get reimbursement for other medical expenses, such as prescriptions or doctor visits. A limited MERP can help keep medical costs contained.

Integrating MERPs With Existing Insurance

Companies can integrate MERPs with existing insurance to adopt less expensive plans with a higher deductible as the base health insurance and use the MERP to bridge the coverage gap. As a result, companies save significantly while still providing exceptional coverage for their employees.

Integrating MERPs with group health insurance plans has the following benefits:

- Fewer administrative burdens: The MERP administrator handles verification and approval of medical expenses, allowing employers to focus on core business operations.

- Cost control for employers: Employers set yearly limits for each employee, allowing them to predict and control the company's healthcare costs effectively.

- Financial relief for employees: A MERP provides an additional layer of protection that helps offset out-of-pocket costs and high deductibles. Workers can seek the medical services they need without worrying about expenses.

Combining MERPs and HDHPs is a winning combination for employers and employees. Although HDHPs can help employers reduce their healthcare costs, the high deductibles can be a burden for workers, especially those who need frequent medical care. Employers can pair a MERP with an HDHP to enjoy the savings of a high-deductible plan while still offering their employees the benefits of a low-deductible plan.

Tax Implications of MERPs

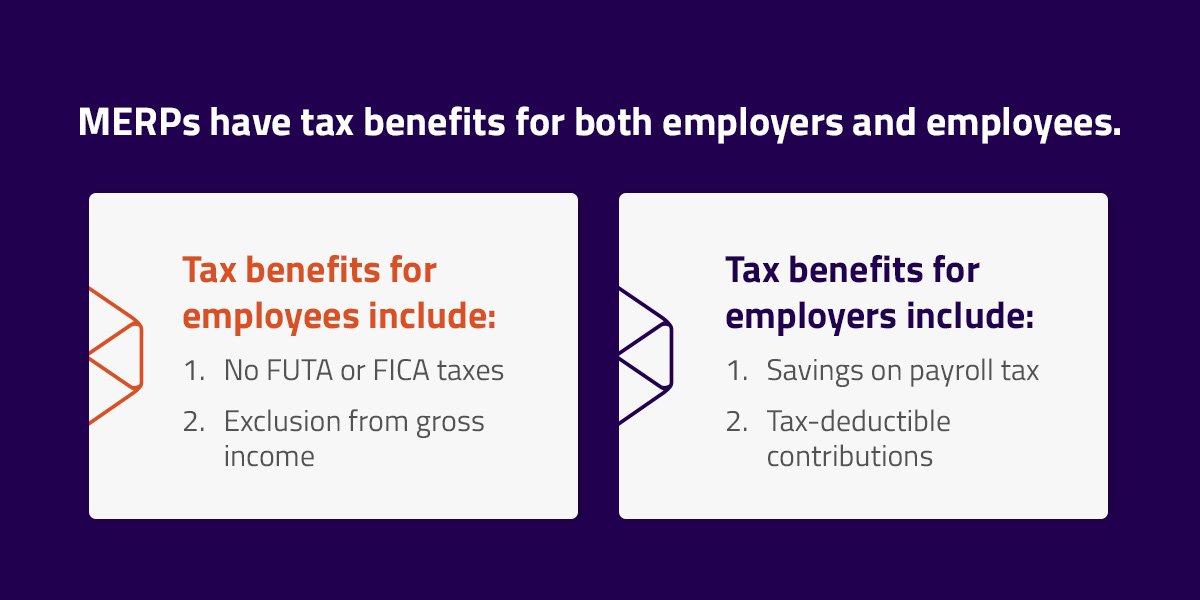

MERPs have tax benefits for both employers and employees. However, MERPs should be managed carefully to ensure compliance with tax laws.

Tax benefits for employees include:

- No FUTA or FICA taxes: Medical expense reimbursements are not considered wages, so they are not subject to the Federal Unemployment Tax Act (FUTA) or Federal Insurance Contributions Act (FICA) taxes.

- Exclusion from gross income: Workers don't have to include the reimbursements in their gross income.

Tax benefits for employers include:

- Savings on payroll tax: Because employer contributions are not considered taxable income for employees, they aren't subject to payroll tax. Employers enjoy additional savings from this benefit.

- Tax-deductible contributions: The amounts employers contribute to MERPs are tax-deductible as a business expense.

Companies that wish to continue enjoying these tax benefits must ensure the MERP strictly adheres to IRS guidelines regarding documentation requirements, eligible expenses and nondiscrimination rules. Workers should also maintain accurate records of their medical expenses and reimbursements, which may be required for tax verification.

Who Qualifies as a Dependant?

Employees can use their MERP funds toward medical expenses accrued by their dependants, such as spouses and children. However, there are rules about who qualifies as an eligible dependant. Under federal regulations, domestic partners and their children, if they are not also biological or adopted children of the employee, are not considered dependants. The same rule applies to other individuals an employee may support financially but who don't meet the technical definition provided in tax codes.

Compliance and Reporting Requirements

Employers implementing MERPs must understand and comply with specific legal requirements. The plans are regulated by various federal laws, including the IRC, the Affordable Care Act (ACA) and the Employee Retirement Income Security Act (ERISA). By complying with these regulations, employers and employees are protected. Compliance also ensures that MERPs provide the intended tax benefits.

Crucial legal aspects to consider:

- ACA compliance: MERPs must comply with the ACA's market reforms. To avoid penalties, MERPs must be integrated with a group health plan that meets ACA minimum essential coverage standards.

- ERISA requirements: Because most MERPS are considered group health plans under ERISA, they must comply with ERISA's disclosure and reporting requirements. Companies are required to file annual reports with the federal government and provide participants with detailed descriptions of the plan.

- Nondiscrimination rules: Under the provisions of the IRC, MERPs must not discriminate in favor of highly compensated or high-ranking employees regarding eligibility or benefits.

These laws and regulations may change over time, and employers must always review their MERPs to ensure compliance with current laws and regulations.

Engaging MERP Administrators

Companies may engage a MERP administrator to maintain a boundary between plan administration and employer responsibilities. The administrator is responsible for overseeing the daily operations of the MERP. For example, the administrator verifies charges, relieving the employer of this task to focus on other business functions.

The MERP administrator ensures that only qualified medical expenses are approved for reimbursement by the company. They check the submitted expenses against the plan's guidelines and engage employees to rectify any discrepancies noted in the verification process.

Workers may receive a dedicated MERP card to simplify the payment process. Instead of paying out-of-pocket for medical expenses and then waiting for reimbursement, employees can use the card to pay directly for healthcare services. The card is preloaded with the employee's allocated funds. The MERP administrator is responsible for loading funds onto the MERP cards and coordinating transactions.

Explore MERP Options With The Difference Card

Employers seeking more cost-effective health plans should consider MERPs. Besides the insurance savings, MERPs have several tax benefits for both employers and employees. We can help you implement MERP in your business or company.

Since 2001, The Difference Card has helped organizations build the most cost-effective healthcare plan, providing our clients an average net savings of 18%. We have delivered millions of dollars in savings to our clients while providing the highest level of employee benefits. Whether you're an insurance broker or employer interested in MERP offers from a reliable partner, you can request a proposal today.