What’s the Difference Between a MERP vs. HSA?

Table of Contents

Health insurance is a major consideration for employees. Businesses looking to hire and retain the best talent need to offer competitive benefits to motivate their team. But how do you offer affordable healthcare without driving up your expenses? Insurance producers can provide businesses with alternative insurance packages to make it easier to offer their employees health insurance at a more affordable rate.

A Medical Expense Reimbursement Plan (MERP) and a Health Savings Account (HSA) are two options for groups looking to manage healthcare costs. With average employer expenses rising to over $15,000 per employee, businesses need cost-effective solutions more than ever. Understanding MERP and HSA options lets you find the best fit for a company's healthcare strategy.

What Is a MERP?

A MERP is an employer-funded, IRS-approved program that reimburses employees for some of their healthcare costs. It's a type of Health Reimbursement Arrangement (HRA). Instead of paying higher premiums for health plans, employers can use a MERP to cover out-of-pocket expenses tax-free. Employers set up a plan that lays out what medical expenses are covered. They set reimbursement limits, eligibility rules and in-network providers. Employees who need medical services get paid out of the MERP for their covered expenses. Employers can write off this payment, and employees get tax-free funding for their medical costs.

What Is an HSA?

An HSA is a personal savings account for medical expenses. Businesses ensure their employees are enrolled in a High-Deductible Health Plan (HDHP) so they can open an HSA. The HSA lets employees put aside pre-tax money for medical expenses like doctor visits, prescriptions and deductibles.

HSA accounts are a great option for employees looking to roll funds over year after year. Unlike employer-funded MERP options, employers and employees can fund HSA accounts. HSA accounts are also tax-deductible and have tax-free growth and medical expense withdrawals. An HSA account gives employees more control over their healthcare spending and savings.

MERP Benefits

A MERP is a more flexible way for businesses to offer employees healthcare coverage. Traditional insurance plans come with fixed costs. A MERP lets employers offer reimbursements for certain medical needs, creating a set medical budget for employees without the high insurance premiums. A MERP benefits brokers and their business clients, creating a more convenient, cost-effective solution for everyone.

Flexibility

One of the biggest advantages of a MERP is its adaptability. When they create the MERP, employers get to choose which expenses to reimburse. Companies can structure their healthcare benefits to meet their budgets while still covering essential employee costs. Instead of sticking to rigid health plans, businesses can use a MERP to fit their workforce. The more comprehensive coverage you want to provide, the more you can budget into your MERP.

Reducing Costs

A well-designed MERP can significantly lower a company's healthcare expenses. Employers can offer lower-premium health insurance plans, like high-deductible options while using the MERP to reimburse employees. Businesses get lower fixed premium costs while still supporting employees. Since MERP reimbursements are only made when employees have medical expenses, there's less unnecessary spending.

Easy Integration

A MERP can easily integrate with different health plans. A business might pair a MERP with an HDHP to manage premium costs and deliver health coverage. Other companies might structure a MERP to work with an HSA, maximizing everyone's savings. Choose a MERP for competitive healthcare while remaining cost-effective.

MERP vs. HSA Comparison

Both MERP and HSA options help employers and employees manage healthcare costs, but they function differently. A MERP is an employer-funded reimbursement plan designed to offset employee medical expenses. HSA are employee-owned savings accounts that grow over time. Choosing the best option will depend on the business. Here's a breakdown of these options to help you find the best option for your business or client:

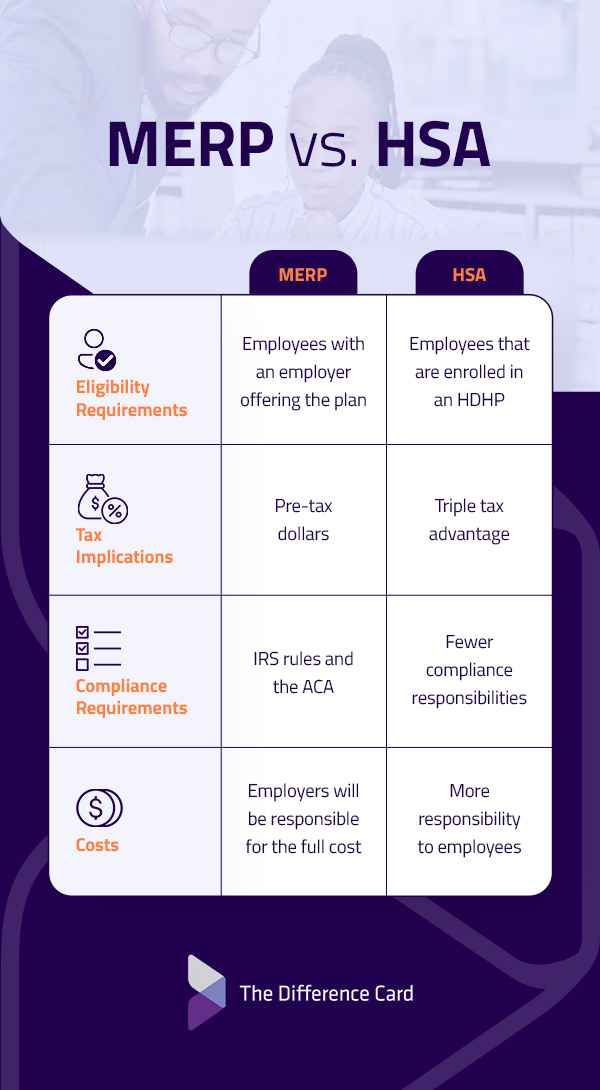

1. Eligibility Requirements

MERP and HSA options have different requirements. A MERP is available only to employees with an employer offering the plan. The employer designs the plan and what it covers, including all medical deductibles, copays and out-of-pocket expenses. There are no contribution limits because the MERP is employer-funded. The business chooses its reimbursement amounts when it creates the MERP. Employees are directly reimbursed through the employer's MERP.

On the other hand, employees qualify for an HSA when they're enrolled in an HDHP. The HDHP sets a minimum deductible for individuals and families. Unlike a MERP, employers and employees can contribute to the HSA. Individual contributions are capped at $4,150, while families get a limit of $8,300. Also, an HSA lets employees use the funds for a wider range of medical expenses than a MERP, as long as they meet IRS guidelines.

2. Tax Implications

Taxes are a major part of any decision. Insurance brokers need to offer businesses solutions that fit their budgets, and taxes can significantly impact any budget. Both MERP and HSA health options come with tax advantages, but they offer them in alternate ways.

Employers fund MERP with pre-tax dollars. This pre-tax funding means reimbursements are not taxable income. Employers also benefit because MERP contributions are tax-deductible business expenses, reducing their overall tax liability. However, a MERP does not allow direct, pre-tax employee contributions, so there are no tax savings beyond the tax-free reimbursement.

An HSA offers a triple tax advantage. Employee contributions are pre-tax, reducing taxable income. Funds grow tax-free, and withdrawals are tax-free as long as they're used for qualified medical expenses. Unlike a MERP, HSA funds roll over indefinitely, making them a valuable long-term savings tool. Employers who contribute to employees' HSA can also deduct those contributions from their business taxes.

3. Compliance and Reporting Requirements

Employers offering a MERP must ensure the plan complies with IRS rules and the Affordable Care Act (ACA). A MERP typically requires formal plan documents to avoid inconsistencies in reimbursements. Employers must also follow nondiscrimination rules to ensure all employees receive benefits fairly. If a MERP reimburses insurance premiums, it might need to comply with additional regulations under the Employee Retirement Income Security Act of 1974 (ERISA).

Employees own an HSA, so employers have fewer compliance responsibilities. Businesses just need to make sure only employees with an HDHP participate. Employers also need to watch their contributions to keep them within IRS guidelines. Employees should report all HSA contributions and withdrawals on their tax returns.

4. Costs

Cost is another major factor for brokers and businesses to consider. If you're looking at a MERP, employers will be responsible for the full cost. While employees pay nothing out of pocket for a MERP, businesses need to budget for reimbursements and administrative fees. A MERP can still be cost-effective because it lets companies offer lower-premium health plans while covering out-of-pocket costs. A MERP also only sees expenses when an employee uses the benefits, instead of businesses regularly paying insurance premiums.

An HSA shifts more responsibility to employees. They do most of the pre-tac contributions unless employers want to contribute. An HSA gives employees long-term savings opportunities, but they have to cover their medical expenses upfront until they grow their HSA. This setup means an HSA has lower administrative costs for businesses than a MERP. However, employees need an HDHP, which has higher expenses before insurance coverage kicks in.

Can You Have a MERP and an HSA?

You can have a MERP and an HSA, but businesses need to structure the MERP carefully. First, your employees would need an HDHP to get access to an HSA. Then, the business would have to structure the MERP only to cover a limited range of medical expenses. The MERP would cover HSA-exempt expenses, such as vision, dental and preventive care services. Businesses could also establish a MERP that only reimburses medical expenses after the employee meets their HDHP deductible.

Offering MERP and HSA options for employees can help businesses design the most cost-effective plan for their needs. However, designing a properly structured plan takes careful planning, often with an insurance broker, to avoid disqualifying employees from an HSA.

Choosing the Right Option for Your Needs

Whether you want a MERP, an HSA or a combination, you need to understand your client or business first. Every business has unique goals, budgets and workforce needs. Some employees might prefer the control an HSA offers them, while others want the administrative work to be out of their hands.

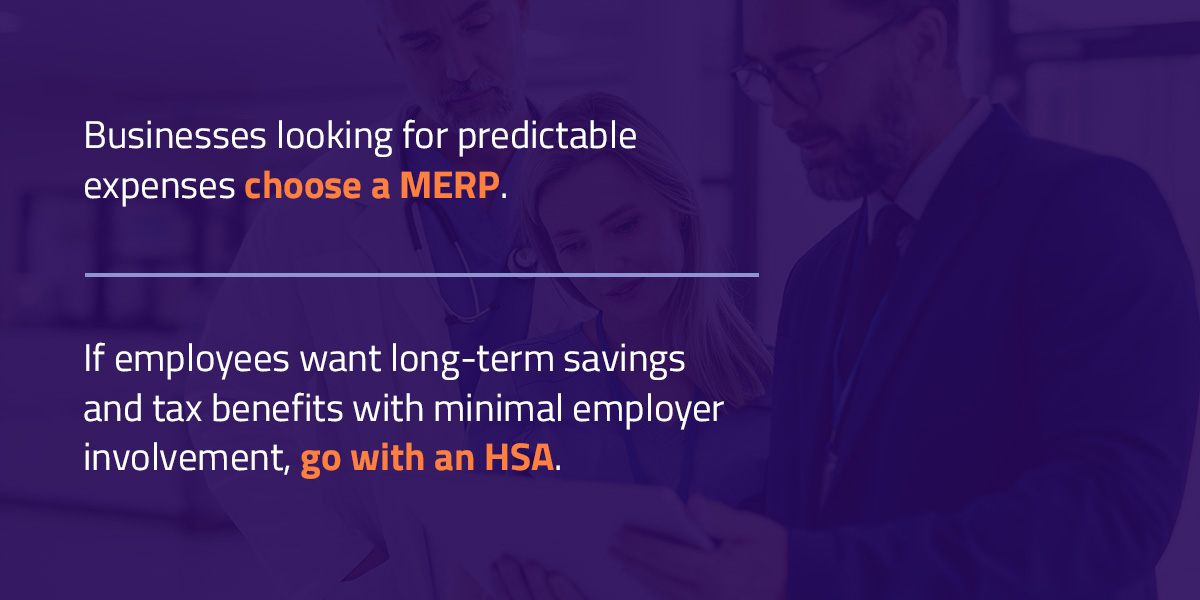

Overall, businesses looking for predictable expenses choose a MERP. If employees want long-term savings and tax benefits with minimal employer involvement, go with an HSA. Businesses can offer both, but it involves a well-structured MERP. Weigh these factors to find the right fit for your operation:

Budget

Cost control is a major influence on the plan a business chooses. Companies should consider a MERP if they want to cover employee medical expenses without committing to high insurance premiums. Costs will fluctuate based on employee claims, which can make it harder to predict expenses. Businesses can set fixed reimbursement limits to help control this unpredictability. However, a MERP is a great way to help out employees since they don't contribute to the fund.

An HSA shifts more responsibility onto employees. They need to enroll in an HDHP and set aside funds for the health account. Going with an HSA means employers provide employees with a long-term health savings plan without the direct responsibility of reimbursing claims. Employers get more tax benefits but often face higher out-of-pocket costs due to their HDHP enrollment.

Employee Needs

Every business needs to consider its employees. Whether you're helping a company choose the right healthcare support or looking to boost employee benefits without increasing costs, you need a plan that people will want to participate in.

If employees are used to low-deductible plans and expect employers to help cover expenses, a MERP will do a better job. Choosing a MERP lets you bridge the gap between affordable premiums and comprehensive coverage without shaking up your system too much. MERP are more flexible, letting you tailor reimbursements to employee needs.

On the other hand, an HSA is better if employees want to take control of their healthcare spending with minimal input from their employers. An HSA lets them save for future needs and cover their current costs. An HSA rolls over yearly, so younger employees with fewer health needs can build a buffer for their future medical services. The HSA's tax-free growth makes them appealing to employees looking for long-term savings.

Administrative Demands

Going with a MERP or an HSA means taking on different administrative loads. Businesses with a MERP will have to manage plan documents, IRS and ACA compliance and discrimination policies. However, businesses have more control over the MERP, so they can easily design the plan to fit their budget and compliance needs.

Employees own their HSA, so businesses have fewer compliance responsibilities. Employers just need to make sure only eligible employees with HDHP enroll. It's employees who are responsible for managing their accounts and reporting contributions and withdrawals on their tax returns. If you're looking to offer an HSA to employees, you might need to provide educational materials so they understand the account.

How The Difference Card Helps Businesses and Brokers

Navigating healthcare options can be complicated, but The Difference Card simplifies the process. Insurance producers and employers get access to a cost-effective, flexible solution designed to reduce costs while maximizing employee benefits.

Brokers can lean on The Difference Card when they need an expert sales tool. They can offer clients customized benefits solutions that lower premium costs and maintain employee benefits. The Difference Card platform seamlessly integrates with existing health plans, providing clients with a healthcare option that stands out. It even provides easy-to-use quoting tools, compliance support and ongoing client assistance.

The Difference Card helps employers control healthcare spending without shifting more costs to employees. Whether you're using an HRA or MERP setup or an HSA system, your employees can swipe The Difference Card to offset their medical expenses. Employers fund The Difference Card account, and employees use the card to pay for part of their medical costs. Employee health insurance covers some, they pay a little and The Difference Card makes up the rest. Businesses can even simplify their administrative costs since they avoid managing complex reimbursement plans.

Find the Right Healthcare Solution With The Difference Card

Choosing between a MERP and HSA isn't your only healthcare option. Businesses can save money and ensure their employees get health coverage with The Difference Card. We create customized healthcare solutions that reduce your costs without sacrificing benefits. Whether you're looking to optimize a business's current plan or explore new cost-saving options, The Difference Card is here to help.

Get your proposal today and take care of your healthcare spending with The Difference Card.